By Mauro Nogarin

Although political stability faced a very tough time due to massive work stoppages in recent months and an increase in taxes, the Central Bank of Colombia in its latest financial report projected an increase of 7.5% to 8.6% in the growth of the Gross Domestic Product for this year; and for 2022, the agency estimated an increase of 3.9% with an inflation of 3.5%.

Also, the construction sector began to rebound at the end of the year, despite the crisis experienced during the first months of 2020 due to the pandemic.

According to the Index of Housing Construction Costs-ICCV published by Colombia’s national statistics institute (DANE), the price of iron and steel inputs registered an annual variation of 40.6%, being the highest price increase in the construction supply chain in the past year. This new 40.6% annual increase in the price of steel accumulates a variation from January 2020 to August 2021 that already amounts to 45.3%, thus hindering the positive trend in this sector.

Construction Sector

However, to compensate for this negative factor, the construction sector benefited from the new fiscal policy of the national government in coordination with the banking system, which have been implementing fiscal incentive measures such as the Frech No VIS, the Plan de Alivio a Debtors (PAD), and mortgage loan guarantees.

The construction of road infrastructure in the country has also had a significant recovery in 2021, as was indicated by a recent analysis by the specialized market research agency Corficolombiana.

According to this study, the recovery of the sector is supporting the good performance of 4G highway concessions, replacing public works that currently continue to lag behind.

At the national level the development of road infrastructure in the month of July, according to the report, registered a growth of 2.9% since January compared to the same period of 2020.

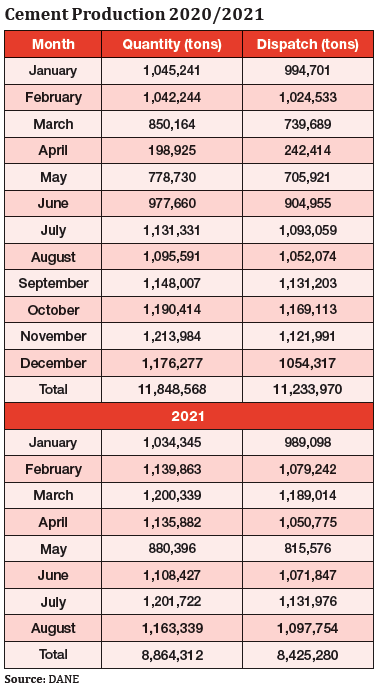

Cement

Also the production of cement, at the national level, is following a positive trend with 1,163,300 tons produced in August, which represented a growth of 6.2% in relation to the same month of 2020, according to the new report published by DANE.

When comparing the month of analysis with the same period of 2019, the production of gray cement at the national level registered a decrease of 1.0%, going from 1,175,000 tons to 1,163,300 tons.

In August 2021, 1,097,800 tons of gray cement were shipped to the national market, which meant a slight decrease of 0.1% compared to August 2019 when 1,099,300 tons were shipped.

In the period from January-August 2021, the production of gray cement reached 8,864,300 tons, registering an increase of 24.5% compared to the same period of the previous year. Shipments to the domestic market accumulated 8,425,300 tons, resulting in a positive variation of 24.7% compared to the period January-August 2020.

In the period from September 2020-August 2021, gray cement production totaled 13,593,000 tons, registering a growth of 16.6% compared to the same period of the previous year. On the other hand, gray cement shipments to the domestic market reached 12,901,900 tons, presenting a variation of 16.1% compared to what was registered in the period September 2019-August 2020.

In August 2021 compared to the same month of 2020, the total result of gray cement shipments was mainly explained by growth from the concrete companies (14%) and Constructors y Contractors (6.5%) channels, which totaled 3.9 percentage points to the total variation of 4.3%.

When comparing the month of analysis with the results obtained in August 2019, gray cement shipments presented a variation of -0.1%, this variation is explained by the decrease of the concrete companies (-6.5%) contributing with -1.5 percentage points.

Prices

Regarding cement prices, according to a new Bancolombia report, despite the strong growth in production, the curve shows a certain stability reaching 2016 levels. And the outlook until the end of 2021 confirms that this trend will remain the same.

Although 2021 was a year in which a good performance was registered in the cement industry, achieving important productive objectives thanks to the strengthening of the domestic market, investments to increase installed capacity did not advance. The uncertainty generated by the pandemic and the political agenda to elect a new president in May 2022 also affected the main cement companies operating in the country.

In fact, the option to increase cement production was rewarded by the results confirmed by companies such as Argos, which increased its growth by 40% with a 38% market share, selling 2.4 million tons through October, followed by Cemex with a 43% increase and a 26% market share.