The Cement Industry In Brazil Expects Flat Growth In 2022, Higher Inflation.

By Mauro Nogarin

According to the new statistical bulletin published by the Central Bank of Brazil, the economy in 2022 will be marked by difficulties due to lower incomes, and the market expects a growth of close to 0.5% of the Gross Domestic Product (GDP).

On the other hand, the Brazilian Communication Agency stated that the financial market has once again raised its inflation forecast for this year, and according to the Broad Consumer Price Index (IPCA), it should close 2022 at 5.38%.

In the real estate market, according to the forecast by the Brazilian Chamber of the Construction Industry (CBIC), the prospects for demand in 2022 will be more cautious.

The construction of luxury houses will continue at a good pace, but on the other hand, the popular housing program “Casa Verde e Amarela” did not meet the expectations announced by the government, thus generating less cement consumption.

However, the return on investment in infrastructure works by the government will be essential in the next 12 months to sustain cement consumption, also considering that the vaccination campaign for construction workers has made considerable progress in the second half of the year.

In fact, the Ministry of Infrastructure wants to auction in 2022, the last year of the current government, works for $31,000 million in investments from the private sector. The amount is almost double what was guaranteed in the first three years of Jair Bolsonaro’s term, when between 2019 and 2021 works worth $14.8 billion were assigned.

Among the outstanding infrastructure works are 14 projects for the concession of 8,800 highways, the delivery of 16 airports and 24 maritime terminals.

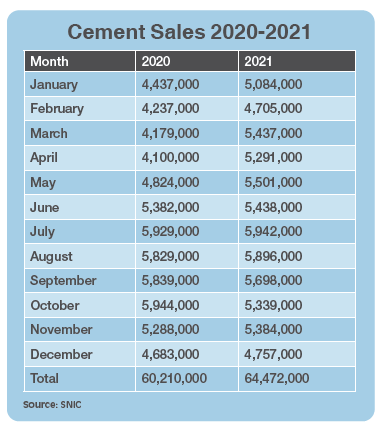

According to the new statistical report of the National Union of the Cement Industry (SNIC), cement sales in Brazil in December 2021 totaled 4.8 million tons, 1.6% more than in the same month of 2020.

With this result, the sector closes 2021 with a total of 64.4 million tons of cement sold, which is 6.6% more than the previous year.

The main factors that boosted the growth of the cement industry were the continuity of the construction sector as a whole, as well as the homebuilding segment and the resumption of infrastructure works.

The participation of concrete companies also showed a positive trend, registering an increase from 18.2% to 18.9% of cement sales thanks to the promotion of private real estate works. But also the prefabricated concrete industry registered an increase in its participation, going from 20.6% to 22.3%.

A year ago, when the pandemic was at its peak, SNIC forecast that sales would expand by 1%, and subsequently rose to 3%. However, as of May, when sales volumes were consolidated, the year ended with a growth of 1.6%, reaching 4.7 million tons compared to the same month of the previous year.

The cement industry in the country currently has 91 factories with an installed production capacity of 94 million tpy, with an idle capacity of 31%, of which the companies still have 11 paralyzed production units.

As for prices, according to the National Civil Construction Index (Sinapi), it had an inflation rate of 1.07% in November 2021, a rate higher than that of October (1.01%). Compared to November 2020, however, there was a decrease, since, in that month, inflation had been 1.82%.

With the November result, Sinapi assumes an inflation of 18% in the year and 20.33% in 12 months, where although construction materials rose 1.66%, the price of a 50-kg bag of cement remained stable throughout the year. The price went from $5.31 in the month of January 2021 to $5.68 in November, registering an increase of 6.9%.

In 2021, with an investment of $40 million, Votorantim Cimentos expanded its facility in Pecém. It was the highest investment in the cement industry sector in Brazil. The new production line of the Pecém cement plant was inaugurated in November in the state of Ceará. With the expansion of this unit, the company now has a production capacity of around 1 million tpy of cement.

The production of the new unit will strengthen the market offering in the metropolitan region of Fortaleza.

Potential for Reducing Carbon Emissions from the Brazilian Cement Industry by 2050

Cement is a fundamental input in the production chain of the construction industry, a basic component of concrete and mortar and the most used man-made material on the planet.

It is also an essential element for the development of infrastructure in the country, which is currently deficient. Cement is the basis for the construction of houses, schools, hospitals, roads, railways, ports, airports, sanitation and energy works, among many others that provide health and well-being to the population and meet the demands of modern life.

Brazil, as a developing country, has an important infrastructure program to be implemented, and the increase in population, combined with its increasing urbanization patterns, should boost the demand for cement in the coming decades.

The cement production process is intensive in the emission of greenhouse gases. The cement industry globally accounts for about 7% of all carbon dioxide emitted by man. Despite this, in Brazil, largely due to a series of actions that the sector has been implementing for years, this share is around 2.6%.

In particular, Brazil is one of the countries that emits the lowest amount of CO2 per ton of cement in the world. This outstanding position, while recognizing the sector’s efforts to combat climate change, represents an enormous challenge: to produce the cement necessary for the country’s development, while seeking solutions to further reduce its emissions of CO2.

With this in mind, the national cement industry, in collaboration with the International Energy Agency (IEA), the International Finance Corporation (IFC) of the World Bank, the World Business Council for Sustainable Development (WBCSD) and a select group of important universities and technological centers in the country, coordinated by professor and former minister José Goldemberg, developed a Cement Technology Roadmap.

It presents different alternatives for mitigating emissions from the domestic industry in the short, medium and long term, capable of reducing industry emissions by around 35% by 2050. With this, adapting to scenarios consistent with the one with the lowest climate impact, will limit the rise in global temperature to up to 2°C.

The study also identifies barriers or bottlenecks that limit the adoption of these alternatives and, based on that, proposes a series of recommendations for public policies, promotion instruments, regulations, normative aspects, among others, capable of enhancing the reduction of emissions in the sector and accelerate its transition to a low carbon economy.

Source: The National Cement Industry Union

Mauro Nogarin is Cement Products’ Latin American correspondent.