It Is Essential To Examine How Major Rail Carriers Operate Across Different Regions In North America To Meet Growing Demand.

By Jake Tanner

While rail currently handles about 10% of aggregate transportation, its role is expanding as companies seek more efficient and cost-effective ways to move massive quantities of materials over long distances. The aggregate industry will fundamentally have a growing dependence on rail transport for several compelling reasons.

Rail offers unmatched efficiency and cost-effectiveness in moving large quantities of heavy materials over extended distances. Compared to road transport, rail can significantly reduce costs over long distances, a critical factor given the immense weight and volume associated with aggregate materials. Rail’s efficiency becomes increasingly advantageous as shipment distances grow, offering significant cost savings over long hauls compared to truck transportation.

According to Matt Culver, senior marketing specialist at RSI Logistics, “Freight trains can move one ton of goods approximately 470 miles on a single gallon of fuel, compared to trucking’s approximately 134 miles per gallon of diesel. This makes rail three to four times more fuel-efficient than trucks.” As derived from that factor, shorter rail shipments often incur higher costs per ton-mile, emphasizing the need for strategic logistics planning to maximize the benefits of rail transport.

Moreover, rail transport provides notable environmental advantages. It produces considerably lower greenhouse gas emissions per ton-mile compared to trucks, a benefit that aligns well with the increasing prioritization of sustainability across industries. In today’s environmentally conscious world, these attributes make rail transport not only an operational necessity but also a strategic choice for aggregate companies seeking to reduce their carbon footprint.

Rail’s ability to access remote mining locations further broadens the reach of aggregate extraction and competitive transportation. Many of these sites are not connected by adequate road infrastructure, making rail indispensable for opening up resources in otherwise inaccessible areas. Additionally, rail is highly reliable, providing a consistent and weather-resilient mode of transportation that minimizes disruptions in the supply chain. For an industry heavily reliant on timely delivery, this reliability ensures materials can meet the steady and growing demand in construction and infrastructure sectors.

Market Needs and Economic Drivers in 2024 and Beyond

Recent economic trends and market dynamics have further underscored the critical role of aggregates and the necessity of more future rail transport. As of 2024, several key factors are driving robust demand for aggregate materials:

- Infrastructure Investments

The bipartisan U.S. Infrastructure Investment and Jobs Act (IIJA), passed in late 2021, continues to fuel significant demand for aggregates. With billions allocated for highways, bridges, and public infrastructure, rail plays a pivotal role in delivering the raw materials needed to complete these ambitious projects. - Resilient Construction Sector

The U.S. construction market, valued at over $1.7 trillion in 2023, remains a major driver of aggregate demand. While interest rates have posed challenges, the sector’s focus on large-scale infrastructure projects and the sustained need for residential and commercial developments underpin the continued growth of aggregate mining. - Urbanization and Population Growth

Increasing urbanization trends and population growth are fueling housing developments and public infrastructure projects. These trends, particularly strong in regions experiencing population booms like the Sun Belt, create heightened demand for aggregate products, further solidifying the necessity of efficient rail transport. - Environmental and Regulatory Trends

Stricter environmental regulations have pushed industries toward adopting greener supply chain solutions. Rail’s lower emissions profile positions it as a critical partner in achieving sustainability goals, aligning with federal and state environmental mandates. These environmental advantages become greater as mines move further and further out from urban centers. - Industry Consolidation and Efficiency

The aggregate industry has seen increased consolidation, with companies acquiring smaller competitors to expand market share and geographic reach. These consolidated operations will increasingly rely heavily on rail to optimize logistics, creating synergies that enhance cost efficiency and broaden market access. - Geopolitical and Economic Resilience

The ongoing global emphasis on supply chain resilience, amplified by the disruptions seen during the COVID-19 pandemic and geopolitical tensions, has made rail an increasingly favored option for its reliability and scalability. Rail networks ensure aggregate products can reach markets seamlessly even in uncertain times.

Building on the critical role of rail in the aggregate industry, it is essential to examine how major rail carriers operate across different regions in North America to meet growing demand. Railroads vary significantly in their geographic coverage, network density, and market focus, which in turn influence their ability to transport aggregate materials efficiently. Union Pacific (UP) and Burlington Northern Santa Fe Railway (BNSF) dominate the western United States, while CSX Transportation (CSXT) and Norfolk Southern (NS) focus on the eastern U.S. Canadian Pacific Kansas City (CPKC) and Canadian National (CN) play critical roles in cross-border and regional transport, further complementing the major U.S. networks.

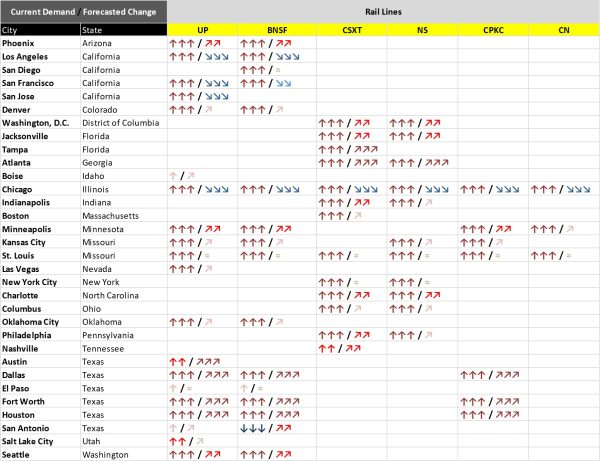

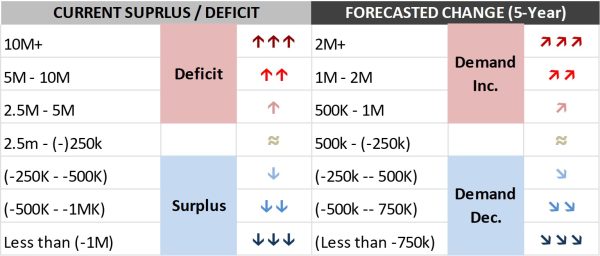

Let’s take a deeper look at the railways and the markets they are near. Provided is a table summarizing which railways have proximity to key markets throughout the United States, specifically reflecting railways that come within proximity of 25 miles from the city center. It also gives insight to Burgex Mining Consultants’ predicted market conditions by comparing production estimates of trucked aggregate supply to estimated per-capita demand. The vertical arrows indicate current market conditions and angled arrows indicating direction of future forecasted demand. The smaller table is the key which is used to interpret the larger data table.

*Example: The first row of the upper table reflecting Phoenix, Ariz., shows that UP and BNSF come within 25 miles from the city center. Under ‘UP’, Phoenix shows over 10+ million tons of demand deficit indicated by the three vertical arrows, and a 1 to 2-million-ton yearly demand increase by 2029, which is reflected by two angled upward arrows.

*Example: The first row of the upper table reflecting Phoenix, Ariz., shows that UP and BNSF come within 25 miles from the city center. Under ‘UP’, Phoenix shows over 10+ million tons of demand deficit indicated by the three vertical arrows, and a 1 to 2-million-ton yearly demand increase by 2029, which is reflected by two angled upward arrows.Comparative Analysis of Aggregate Shipments

A comparative look at Union Pacific (UP) and Burlington Northern Santa Fe (BNSF) Railroads, which dominate the western United States, against CSX Transportation (CSXT) and Norfolk Southern (NS), which are concentrated in the east, reveals distinct market impacts driven by geography and industry focus.

UP and BNSF benefit significantly from their access to the vast resources of the western United States. This region is home to extensive quarries and mining operations, particularly in states such as Arizona, Nevada, Utah and Texas, where aggregate production thrives due to the abundant natural deposits. Additionally, the expansive western network enables these carriers to serve large metropolitan areas like Los Angeles, Dallas and Seattle, as well as booming Sunbelt regions where construction demand is surging due to population growth and infrastructure investments.

The West Coast ports served by UP and BNSF further enhance their strategic advantage. Major urban centers reliant on imported construction materials benefit from rail connections that distribute aggregates inland. For example, aggregates from the Pacific Northwest or inland mining operations can be transported efficiently to support urban development and road-building projects in west coast states such as California. Moreover, these railroads support energy-related projects in the West, such as wind turbine installations and fracking operations, both of which require substantial aggregate materials.

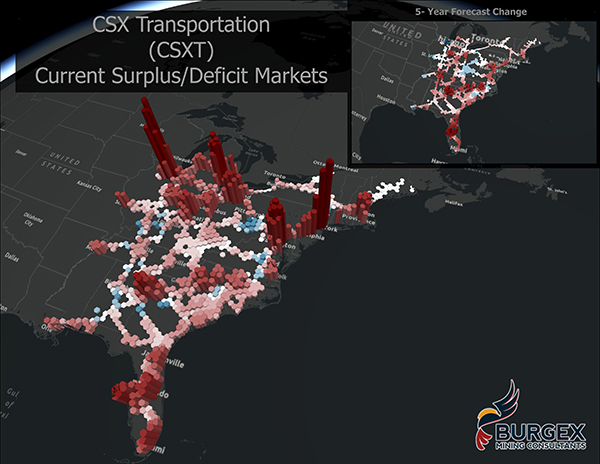

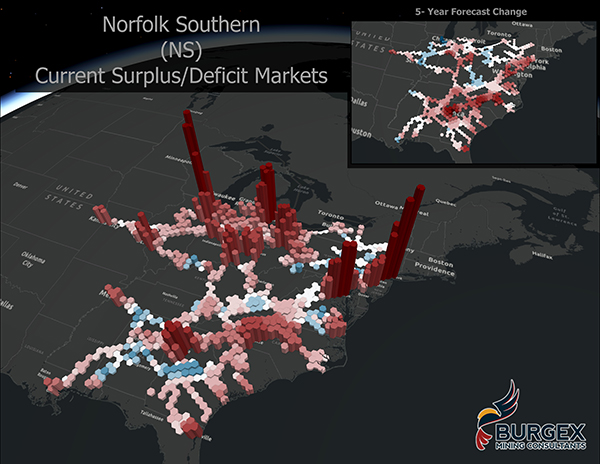

On the other hand, CSXT and NS are the dominant players in the eastern United States, where the transportation of aggregates is influenced by the region’s dense population centers, older infrastructure and manufacturing base. Eastern markets rely heavily on aggregates for urban renewal projects, highway expansions and residential construction, particularly in high-growth areas such as Atlanta, Charlotte and the Northeast Corridor. The Appalachian region also provides a key source of aggregates, with these railroads connecting quarries in Pennsylvania, Virginia and Kentucky to regional and national markets.

Unlike their western counterparts, CSXT and NS operate within denser rail networks, offering greater flexibility to serve smaller or more isolated markets. This makes them well-suited for short-haul aggregate shipments. However, this advantage can turn into a cost disadvantage if shipments consistently occur over short distances, failing to leverage rail’s inherent cost savings for longer hauls.

The interplay between eastern and western carriers is most evident in shared hubs such as Chicago, the largest rail interchange in North America. Here, aggregates and related materials often switch between networks, enabling eastern and western regions to meet their respective construction demands. However, while Chicago represents a key point of overlap, the dominance of UP and BNSF in transporting aggregates across the western expanse contrasts sharply with the more localized focus of CSXT and NS in the east.

Another crucial distinction lies in the commodities’ end-use industries. Western railroads cater to large-scale industrial and energy-related construction, including pipelines, solar farms, and wind energy projects, while eastern railroads focus more on urban and suburban developments.

For instance, aggregates moved by CSXT and NS often support projects tied to urbanization, such as housing developments, while UP and BNSF play a significant role in supplying materials for expansive infrastructure projects like highway corridors and rail expansions across sparsely populated regions.

The geographic and market-specific differences between UP and BNSF in the west, and CSXT and NS in the east, define their respective impacts on the aggregate materials market. While western railroads benefit from natural resource abundance and large-scale infrastructure projects, eastern railroads leverage their dense networks and proximity to growing metropolitan areas. Together, these carriers form a complementary system that ensures the steady supply of aggregates critical for America’s construction and infrastructure needs.

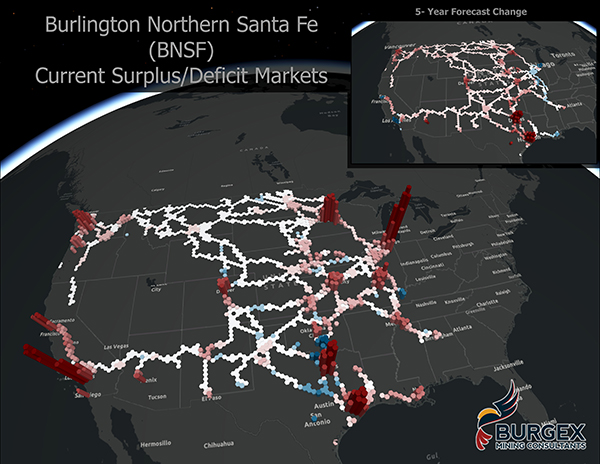

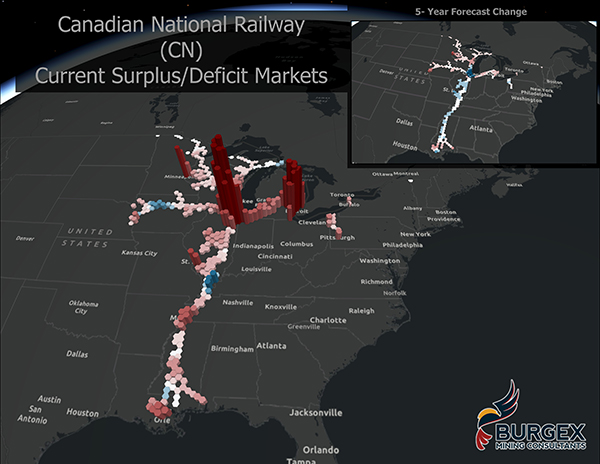

The above maps highlight key U.S. rail lines in proximity to major markets. The color and height of the hexagons correspond to the colored arrows shown in the data table. To emphasize current conditions and better visualize forecasted growth, the height of hexagons are displayed at different scales. These visuals provide valuable insights into opportunities for long-distance product movement across the extensive rail network.

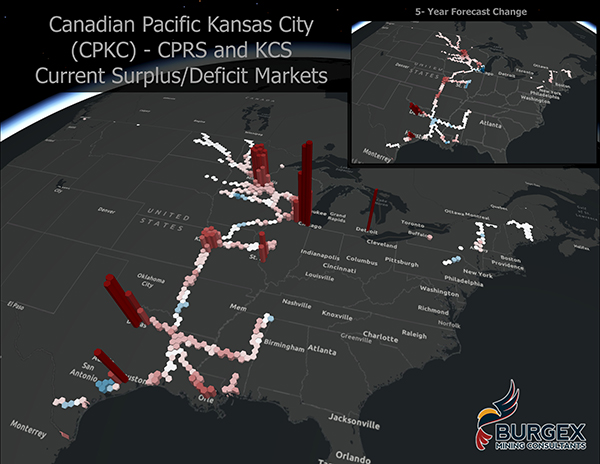

Canadian Pacific Kansas City (CPKC) and Canadian National (CN) play smaller but regionally significant roles in the movement of aggregate materials. While their networks cover less of the U.S. compared to larger railways, they fill critical gaps, particularly in cross-border trade and niche regional markets.

CPKC, formed through the merger of Canadian Pacific and Kansas City Southern, has created a seamless north-south corridor linking Canada, the central U.S., and Mexico. This unified network supports aggregate shipments from resource-rich regions in Canada and the Midwest into high-growth markets in Texas and Mexico.

In Texas, parts of the network rely on leased rail to connect key segments, ensuring access to critical industrial and construction hubs. While its overall footprint is smaller than the major U.S. railroads, CPKC’s strategic focus on cross-border markets makes it a critical player in the aggregate supply chain.

CN connects Canadian aggregate sources to the central and southern United States, leveraging its access to the Midwest, Mississippi River, and Gulf Coast ports. This positions CN as an important conduit for industrial and export-oriented aggregate shipments, though its limited U.S. reach makes it more of a specialized carrier than a dominant player.

CPKC and CN play a crucial role in providing regional and cross-border connectivity for aggregate transportation, complementing the larger U.S. rail networks. However, it’s essential to assess market serviceability, as these rail lines have access to a more limited number of critical U.S. markets compared to their larger counterparts.

Key Analysis Takeaways, Navigating Challenges and Capturing Opportunities

The analysis of aggregate material transportation highlights the strategic importance of rail in meeting the growing demand for construction and infrastructure materials across North America.

Union Pacific (UP) and Burlington Northern Santa Fe (BNSF) Railroads stand out due to their expansive networks, which enable them to capitalize on the vast distances across the western United States. These carriers not only connect resource-rich areas with major urban centers like Los Angeles, Dallas and Houston but also support growth in high-demand regions such as Texas and California. Their ability to efficiently serve both metropolitan markets and remote project sites provides a competitive advantage in the movement of aggregate materials.

CSX Transportation (CSXT) and Norfolk Southern (NS), while less expansive, play a crucial role in providing access to densely populated and economically vital Eastern markets. Their networks connect key cities along the Eastern Seaboard and interior markets, offering reliable service for shorter-haul shipments that are critical for urban development and public infrastructure projects.

Together, these railroads, along with complementary networks like CPKC and CN, form an essential system that supports the aggregate industry’s ability to meet the demands of construction and infrastructure development across diverse geographic and market needs, however their distance of shipment should be greatly considered by nature of their shorter distances than UP and BNSF.

Rail transport is not merely a logistical convenience but a strategic imperative for the future of the aggregate industry. Its unmatched efficiency, cost-effectiveness, environmental benefits, and reliability make it an essential part of the supply chain. As infrastructure spending, construction activity, and urbanization continue to drive demand for aggregate materials, rail transport’s role in supporting this sector is more vital than ever. By leveraging the strengths of rail, the industry can meet the challenges of today’s market while positioning itself for sustainable growth in the years ahead.

Jake Tanner is lead GIS developer for Burgex Mining Consultants, www.burgex.com.