Carbon Capture Is Becoming a Reality In The North American Cement Industry, Albeit With Fresh Headwinds From The Current U.S. Administration. Yet, Significant Structural Challenges Remain To Be Solved Before Industry-Wide Implementation Becomes Possible.

By Jonathan Rowland

Heidelberg Materials’ Edmonton plant is advancing the first full-scale CCS system in the North American cement industry, aiming to capture 1 million metric tons of CO2 annually.

Carbon capture and storage (CCS) is “essential for achieving the industry’s 2050 carbon neutrality goals,” according to Rick Bohan, senior vice president of cement at the American Cement Association (ACA, formerly the Portland Cement Association).

In recent years, there has been a surge in CCS projects in the cement industry worldwide, demonstrating that various technologies are at least technically feasible, if not commercially viable. “I think the jury is still out on what technology will best fit specific plants,” Bohan continued. “In some cases, it may be a question of multiple technologies, for example, amine or cryogenic capture in conjunction with oxyfuel combustion.”

What is not in doubt is that large-scale carbon capture is expensive. Heidelberg Materials’ new Mitchell cement production line in Indiana (with a more than $650 million price tag) is pursuing a full-scale carbon capture system, expected to cost over $1 billion, to capture 2 million metric tons of CO2 annually. “Most corporations don’t have access to that financial wherewithal,” said Bohan. “You’re going to have to look at public financing or alternative funding mechanisms, such as green bonds.”

The cost of carbon capture may indeed become a key competitive differentiator. According to Emir Adiguzel, founder and director of the World Cement Association, carbon capture is “dictating the global cement production map [with] small- to mid-sized companies at risk of disappearing, while large multinationals with access to substantial funding emerge as dominant players.” Finance is also only one of the challenges to implementing carbon capture at scale. Before we get to these, however, a quick look at the current state of play.

Chaos in the U.S.

CCS in the United States was dealt a blow at the end of May, when the U.S. Department of Energy (DOE) abruptly axed $3.6 billion in funding for CCS projects, alleging the previous administration had “failed to conduct a thorough financial review” before awarding the money. This included $500 million for a full-scale CCS system at Mitchell, which has been progressing with geologic testing and design refinement. “The DOE indicates this decision can be appealed, and we are evaluating this course as we consider our next step,” the company told Cement Optimized.

The DOE reversal also reportedly impacts National Cement’s Lebec Net-Zero Project, although this was not confirmed at the time of writing. The project was to receive $500 million in DOE funding, announced at the same time as Mitchell’s award. National Cement is aiming to reach carbon neutrality at Lebec by reducing carbon emissions via alternative fuels and producing a calcined clay blended cement. Carbon capture and storage mops up the remaining 0.95 million tons of CO2 emissions annually.

In response to the DOE’s decision, ACA President and CEO Mike Ireland called the announcement a “missed opportunity for both America’s cement manufacturers and this administration, as CCS projects have long been supported by bipartisan members in Congress and bipartisan administrations, including President Trump’s first term. We stand committed to supporting our members in the appeal process to ensure these critical investments are delivered.”

Other recent recipients of DOE funding include a project to develop a carbon capture, removal, and conversion test center at the Cemex Knoxville plant in Tennessee, which was unaffected by the DOE announcement, Cemex confirmed to Cement Optimized, and a project to create a Carbon Capture Management Innovation Center at the Holcim US Hagerstown cement plant in Maryland. (Ed: Holcim declined to comment for this article, due to the upcoming spin-off of its North American business). As announced in January 2025, both were to receive a share of $101 million from the Office of Fossil Energy and Carbon Management.

Elsewhere, Holcim is pursuing two large-scale carbon capture projects in the U.S., according to the Geoengineering Monitor Atlas, which tracks CCS projects. The Ste. Genevieve plant in Missouri, already the largest in the U.S., is expanding capacity to more than 5.1 million tons annually, with plans to implement CCS as part of the expansion, capturing 2.75 million tons annually by 2028/29. The portland cement plant is expected to capture 1.3 million tons of CO2 annually, starting in 2032.

Calmer Waters in Canada

Meanwhile, large-scale carbon capture projects are progressing north of the border. Heidelberg Materials is advancing the “first full-scale CCS system in the North American cement industry at Edmonton, Alberta,” David Perkins, the company’s senior vice president of sustainability and public affairs, told Cement Optimized. “Once operational, this plant is expected to capture up to 1 million metric tons of CO₂ annually. “

The Edmonton system will integrate CCS with a combined heat and power facility. “With our previous investment in alternative fuels, this could enable the production of carbon-neutral cement,” Perkins continued. “On the storage front, the project team has been working with our storage partner Enbridge to develop this component and has drilled and tested an evaluation well. The project has received strong support from the Government of Canada and the province of Alberta, including a contribution agreement through Innovation, Science and Economic Development Canada (ISED), contingent on final investment decision (FID) approval by our supervisory board.”

The Hedielberg Materials’ Edmonton project is working through final design and engineering refinement and optimization, while continuing to develop the business case and working toward FID. Meanwhile, Holcim’s Exshaw plant in Alberta is progressing a project to capture 1 million metric tons of CO2 annually by 2030, according to the Geoengineering Monitor Atlas.

The Interconnection Challenge: Powering Carbon Capture

Beyond political squabbles over funding, carbon capture faces a complex and challenging road to at-scale implementation. Take the additional power demand needed to capture CO₂. Cement is already an energy-intensive process.

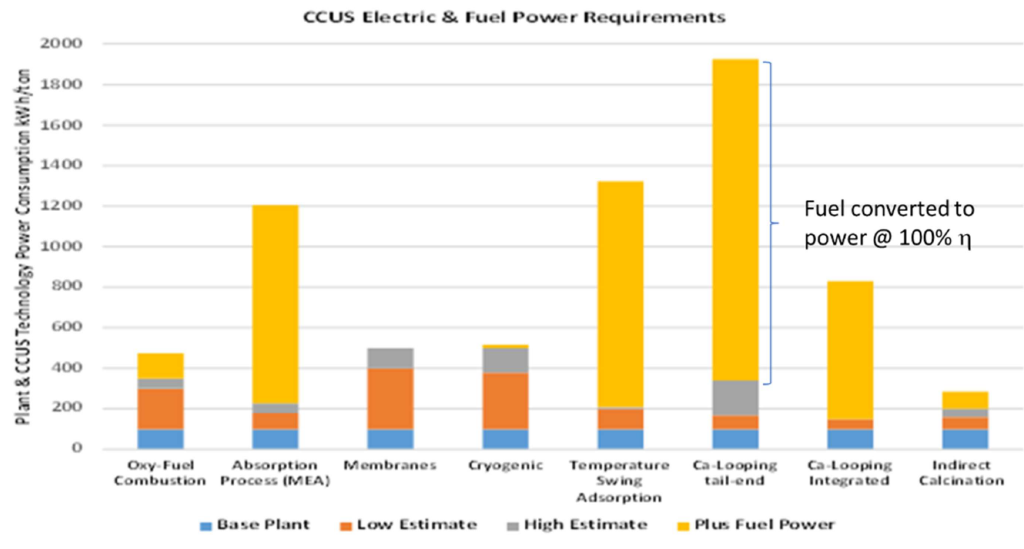

Adding carbon capture to the mix would significantly increase that per-ton energy consumption. Figure 1 shows the base plant power consumption (blue) plus the low (orange) and high (grey) power consumption estimates for carbon capture. The yellow bar on top shows the additional power needed if all heat requirements came from electric power; however, this assumes an optimistic (!) fuel-to-power conversion rate of 100% efficiency.

This raises multiple questions about our ability to supply sufficient clean electricity, especially given a concurrent general push to electrify industrial processes. One often overlooked is the additional burden it will place on the power grid.

Sometimes called “the world’s largest machine,” decarbonization will require the North American power grid to grow even bigger, perhaps costing up to $740 billion, according to the National Renewable Energy Laboratory (NREL). The reason for this grid expansion? “Of the 73.5 quadrillion BTUs of energy consumed by Americans in 2021, less than 20% was provided via electric power,” wrote Brian Potter in a 2024 article for the Institute of Progress. “Decarbonization will require quadrupling electricity generation. An NREL model similarly estimates that reducing emissions by 80% from 2005 levels will require nearly tripling electricity generation by 2050.”

At the same time, continued Potter, “predictable sources of electricity (such as coal plants) are being removed from the grid and replaced by sources like wind and solar, which fluctuate in their output.” These variable generating sources need greater reserve margins to meet demand and, alongside a predicted increase in extreme weather events, will make maintaining grid reliability “more difficult.”

There is also the question of connecting additional generating capacity and large power consumers (such as carbon capture plants) to the grid within the timeframes required to meet decarbonization targets. Writing for Construction Physics, Potter highlights the challenge, noting the so-called “interconnection queue” currently comprises about 11,000 projects.

This queue lists the projects awaiting assessment to determine “whether the existing system has enough capacity to handle the change and what upgrades might help handle the increased load.” Projects passing this evaluation may move to construction and ultimate connection to the grid. However, as the ACA’s Bohan noted, there are practical hurdles here, too, including a lack of electrical engineers and skilled tradespeople.

The good news is that there is currently 1,900 GW of combined generation and storage capacity in the interconnection queue, demonstrating a strong ambition to meet the anticipated growth in demand, and much of this is renewable. However, with wait times so long, “the interconnection queue is a major bottleneck,” concluded Potter.

“We recognize the successful deployment of CCS at scale hinges on the availability of supporting infrastructure, particularly clean energy, grid capacity, and CO₂ transport and storage networks,” Heidelberg Materials’ David Perkins said. “These are not minor considerations. CCS systems are energy-intensive, and without sufficient low-carbon power, the net benefit of capture can be diminished.”

To address these challenges, the company is:

- Advocating for coordinated infrastructure planning with governments and utilities.

- Exploring on-site energy generation options, such as CHP systems, to reduce grid dependency.

- Participating in regional and national dialogues to accelerate permitting and investment in CO₂ pipeline and storage infrastructure.

“We believe the cement industry must work collaboratively – across sectors and with policymakers – to ensure that infrastructure bottlenecks do not stall CCS deployment,” Perkins concluded. “Public-private partnerships and regulatory certainty are critical enablers.”

Where Do We Put The Carbon?

Having captured the carbon, the next question is, what do we do with it? “The Holy Grail would be to take CO₂ and turn it into a saleable product,” said Bohan. There are steps in this direction. St Mary’s Cement has demonstrated using untreated cement stack emissions in a photobioreactor, where fast-growing algae consumes CO₂, creating usable biomass. According to the company, the algae is suitable for producing various valuable materials, such as biofuels, soil amendments, pharmaceuticals, and nutritional supplements.

Meanwhile, companies like Blue Planet and Carbon Upcycling use captured CO₂ to manufacture artificial supplementary cementitious materials. CO₂ can also be used to cure precast concrete. “I would like to see far more research done into carbon utilization,” continued Bohan. “However, what often holds people back is that CO₂ is the lowest energy state possible, so to turn it into usable materials would require a tremendous energy input, which circles us around to the challenges of clean energy and the power grid mentioned earlier.”

“While geological storage remains the most mature and scalable pathway for CO₂ sequestration, we continue to monitor and see the need for and potential in utilization technologies,” said Heidelberg Materials’ Perkins. “These include mineralization, synthetic fuels, and concrete carbonation, among other technologies. We are exploring various opportunities to integrate utilization that aligns with our product portfolio and sustainability goals. That said, utilization alone will not be sufficient, at least in the near term, to meet the required scale of emissions reductions. It should be viewed as a complementary strategy to storage, particularly in regions where storage infrastructure is limited or still under development.”

On the geologic storage question, “most cement facilities in the U.S. are not co-located with suitably deep geologic CO₂ storage,” according to Elizabeth Moore and her colleagues in a 2024 paper from the MIT Concrete Sustainability Hub, examining how the cement industry could facilitate widespread industrial CCUS adoption. Therefore, delivering CCUS at scale and cost-effectively “will require the buildout of an extensive carbon pipeline system.”

The research team behind the paper analyzed systems designed to abate four fractions of carbon emissions – 15%, 30%, 60%, and 85% – based on the “lowest total system cost (capture + transport + storage) to achieve that target.” Unsurprisingly, the more carbon captured, the longer the pipeline network required, and the higher the cost. At 15% abatement, just 247 km of pipelines would be needed, compared to 6,864 km in the 85% scenario. However, at 85% abatement, cement-based carbon hubs “could enable capture from ~100 additional industrial sources, capturing five times the emissions for twice the infrastructure investment.”

On carbon injection itself, Bohan reminded us that this may be a “nascent technology for the cement industry. However, the oil and gas industry has been practicing carbon storage since the 1930s in enhanced oil recovery. The cement industry should be able to build on this expertise and experience; however, site-specific studies will be needed to confirm sequestration potential, as is currently happening at the Mitchell site, while questions about who retains legacy liability of sequestration sites still need to be answered.”

Conclusion: CCS Within Sight?

“If you asked me 10 years ago whether I thought cryogenic capture would have any value in the cement industry, I would have laughed,” said Bohan. “Now, I’m looking at it and thinking, wow, that is a viable option. And that’s exciting. We are seeing technologies that were innovative 20 years ago become commonplace today. So, I can see a future where, within five or six years, we have carbon capture established in the cement industry.”

What level will it be? That’s an economic and societal question that still needs to be answered and, as recent developments in the United States have shown, these are controversial issues. “There’s no free lunch,” concluded Bohan. “How much are we willing to pay to capture CO2? Do we capture 95% or settle for something lower but more economically sustainable? These are conversations we need to have. However, we will not achieve carbon neutrality without carbon capture. The American cement industry is committed to achieving this goal, and we have the technologies to achieve it, so I’m optimistic that, despite the challenges, CCS will become a reality.”

Heidelberg Materials’ Edmonton plant is advancing the first full-scale CCS system in the North American cement industry, aiming to capture 1 million metric tons of CO2 annually.